How are firms going to meet client demands for pricing flexibility and transparency without excellent control over every matter budget? Without cost confidence, a firm is at a disadvantage during initial client discussions – especially if a dedicated procurement team is involved. There will be a risk that clients will be offered discounts or a low margin AFA option to win the business – with zero understanding of the downstream impact on profit.

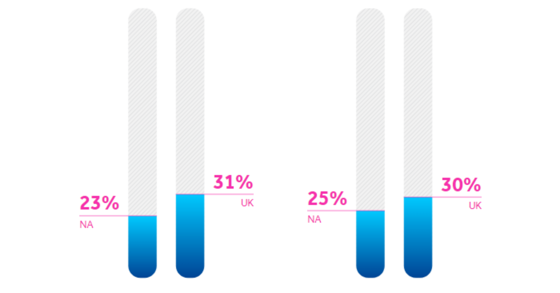

As this BigHand research confirms, inadequate management of matter budget is a concern – firms confirm that lack of matter budgeting (23% NA, 31% UK) and underpricing work initially (25% NA, 30% UK) are contributing to profit leakage.

The dispersed workforce over the past 18 months has also contributed to the problem and preventing firms from allocating the right resource to each matter. As we discussed in Resource Management in a Hybrid Working World, efficient resourcing is important for both internal profitability and to reinforce the client relationship. 22% (NA) and 22% (UK) of firms confirm that failing to use the right resource to complete phases and tasks is adding to profit leakage.

Piecemeal Strategy

Firms are introducing several measures to address these issues, with the majority (80% NA, 67% UK) introducing more mandated matter budgeting since the pandemic began. Policies and processes are not consistent, however, which means clients’ experiences will vary, affecting their overall impression of business value.

There is significant room for improvement: less than 2% (UK) and 3% (NA) firms mandate the use of set budgets for 100% of matters. On average, budgets are used for only 39% (NA) and 36% (UK) of matters; and the cost of allocated resources is included for only 38% (NA) and 38% (UK) of matters when firms are pricing a legal matter.

Questions can also be asked about the effectiveness of this budgeting because the vast majority of firms are not tracking costs against budget. For matters with set budgets, just 2% (NA) and 2% (UK) of firms said they always track actuals against the budget throughout a matter lifecycle. It is interesting to note that for matters that aren’t assigned a budget the numbers are similar: just 2% (NA) and 1% (UK) track costs throughout the lifecycle.

Tracking all costs throughout the lifecycle not only provides the depth of information required to meet client visibility demands – with associated benefits of avoiding late payments and write-offs – but also offers firms vital insight into trends in profitability that can be used to support strategic planning. With the right tools in place to provide this information, firms will be in a better position to enforce the process changes required to implement matter budgeting and tracking for all matters.

This was an excerpt from The Legal Pricing and Budgeting Report. Access the full report to dive deeper into the findings from over 800 legal professionals: